Financially Healthy in the City?

- Shalena

- Dec 20, 2025

- 5 min read

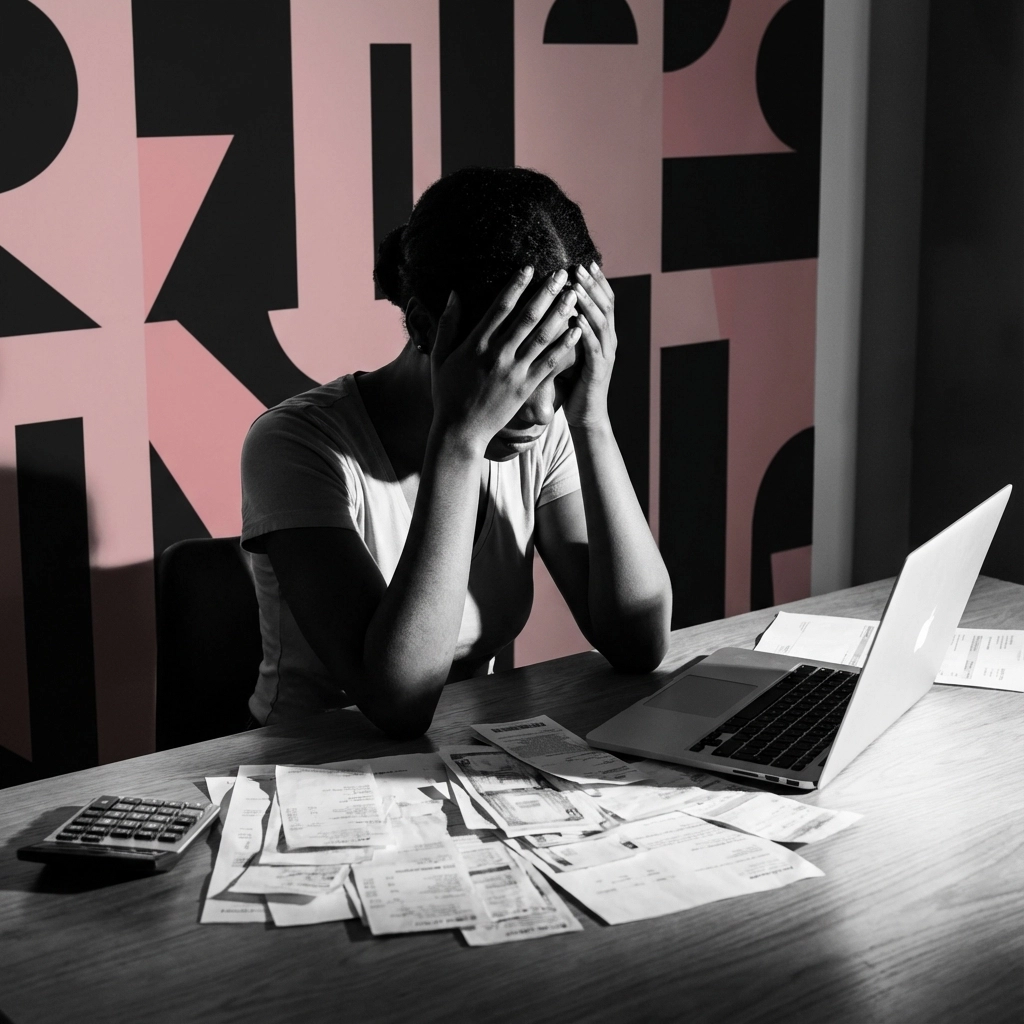

The "financial wellness" conversation is missing one big thing: reality. Everywhere you look, somebody's selling the idea that being "financially healthy" is just a mindset. Like if you manifest hard enough, you can budget your way out of paying $2,000+ rent on a $45K salary.

But here's the tea: if you're a young adult trying to make it in any major city right now, you already know it's not just vibes. It's math. Cold, hard, unforgiving math that doesn't care about your positive affirmations.

Let's be real about what we're working with. According to the Harvard Joint Center for Housing Studies, a record number of U.S. households are now "cost-burdened," spending more than 30% of their income just on housing. For renters? The situation's even tougher. And that's before we talk about groceries that somehow cost more while you're buying less, or student loans that sit on your back like that friend who never pays you back but keeps asking for favors.

Why It Feels Impossible (Spoiler: Because It Kinda Is)

Before we dive into strategies, let's ground this in facts, not shame. The Federal Reserve's 2024 data shows that only 47% of adults ages 18–29 could cover a $400 emergency with cash. That's not because young people are irresponsible – it's because the cost of existing has outpaced income growth for years.

Food prices were up 2.6% in the 12 months ending November 2025, and eating out jumped 3.7%. Meanwhile, Zillow reported the typical asking rent hit $2,007 nationally by August 2025. When your baseline costs eat up most of your check before you even think about savings, "just budget better" becomes about as helpful as "just stop being poor."

The most frustrating part? People love acting like struggling financially is a personal character flaw instead of a predictable result of expensive cities and wages that haven't kept up. That narrative needs to die.

What's Actually Working: Real Strategies for Real Life

Track Every Dollar (But Make It Low-Effort)

Yes, this matters – not because you're financially irresponsible, but because city living comes with sneaky spending leaks. Transit taps, bodega runs, subscriptions you forgot about, "just one thing" purchases that somehow add up to your entire grocery budget.

Here's how to do it without making yourself miserable:

Track every purchase for just 7 days

Don't judge it – just collect data like you're a scientist studying your own life

Circle your Top 3 money drains (spoiler: it's usually food, transportation, and random stress spending)

Instead of obsessing over every penny, try category tracking:

Housing + utilities

Transportation

Food at home

Food away from home

Debt payments

Subscriptions

"Life happens" fund

Your budget can't protect you if it's based on hopes and dreams. It needs receipts.

The 48-Hour Rule That Changes Everything

Here's a game-changer: pause 48 hours on any non-essential purchase. If it's not food, housing, transportation, health, or a bill – wait two sleeps. Most impulse buys don't survive that long, and you'll be shocked how much money stays in your account.

Emergency Funds Start at $50, Not $1,000

Financial advice often acts like everyone can just save three months of expenses immediately. But emergency funds don't start at $1,000 – they start at "something."

The City Starter Emergency Fund:

Begin with $50 (or whatever you can manage)

Auto-transfer $5–$15 every payday to a separate savings bucket

Make it boring – boring is stable

Without an emergency buffer, every surprise gets paid for with credit cards, overdrafts, or borrowing from friends. Those options add stress, fees, and relationship drama fast.

Dealing With the Big Stuff: Student Loans and Real Resources

If student loan payments are drowning you, don't suffer quietly. Look into Income-Driven Repayment (IDR) plans through Federal Student Aid. The rules and availability can change due to court actions, so stay updated on what's available.

The goal isn't to "win" the student loan game overnight – it's to get into the most manageable payment situation possible so you can actually breathe.

When You Need Real Help Right Now

If you're past the point where budgeting tips can help, these are legit places to start:

Housing + Bills: Call 211 for local rental assistance, utility help, and emergency support in your area.

Food Support: Use Feeding America's food bank locator or check your state's SNAP directory if groceries are breaking your budget.

Utilities: LIHEAP can help eligible households with heating, cooling, and energy bills.

Credit Issues: For free credit reports, use AnnualCreditReport.com (avoid the look-alike scam sites). If you can't pay credit card bills, call your card company about hardship options.

The 7-Day City Money Reset

If your finances feel chaotic, try this once. It's a reset, not a lifestyle change:

Day 1: List your non-negotiables (rent, utilities, minimum debt payments, transportation, groceries) Day 2: Track spending for one full day Day 3: Cancel or pause one subscription you don't actively use Day 4: Call one bill provider and ask for a cheaper plan or current promotions Day 5: Set up automatic emergency savings (even $5 per payday counts) Day 6: Choose one "pressure spending" replacement (like planning one takeout day instead of stress-ordering delivery) Day 7: Pick one goal for the next two weeks

Small wins aren't actually small – they build the habit and the confidence you need to keep going.

Money Stress Is Real Stress

Let's talk about the mental health piece nobody mentions enough. Money stress doesn't stay in your bank account – it shows up in your sleep, your relationships, your work performance, and your physical health.

You don't have to announce your financial situation to everyone, but you can normalize real conversations:

"I'm cutting back this month – can we do something low-cost?"

"I'm trying to get my finances tighter. What worked for you?"

"I'm not doing big spending right now. I'm focused on stability."

If someone only likes you when you're spending money, that's not friendship – that's a monthly subscription you can't afford.

The Real Goal Isn't Perfection

Financial wellness content online often sounds like it's written for people who already have disposable income. But if you're in survival mode, your goal isn't "rich" – it's steady.

Steady looks like:

Knowing where your money goes

Paying essentials first

Keeping a small emergency buffer

Reducing chaos fees (late fees, overdrafts, interest spirals)

Asking for help early instead of late

And here's something nobody tells you clearly enough: struggling in this economy doesn't mean you're failing. It means you're navigating genuinely difficult conditions that previous generations didn't face at this scale.

The "financially healthy" conversation needs more honesty about what we're actually up against. It's not easy – it's strategic. And strategy, unlike wishful thinking, actually works.

Want to share what's helping you or what you're struggling with? Drop a comment and let's keep this conversation real. We're all figuring this out together, and there's no shame in admitting that "budgeting your way to wealth" isn't as simple as the internet makes it sound.

Comments